From Underdog to Big Dog: Phoenix Capital Group Touts D-J Basin Deal

In a year of multi-billion-dollar oil and gas deals, Phoenix Capital Group Holdings LLC’s relatively small $33 million acquisition of 4,000 royalty acres in Colorado could easily be overlooked as a drop-in-the-bucket transaction.

But for a company that relishes being the underdog, that’s just fine with them. The acquisition of interests from the city of Thornton is another in a long series of steps the company is taking as it aims to become a “leader in the minerals rights space,” the company says.

Along with ambition, it’s also a company with a leadership that doesn’t mince words, whether it’s calling out “unsavory and, at times, unethical and dishonest mineral shops,” “lowball offers” or celebrating its wins over its better capitalized private-equity competitors.

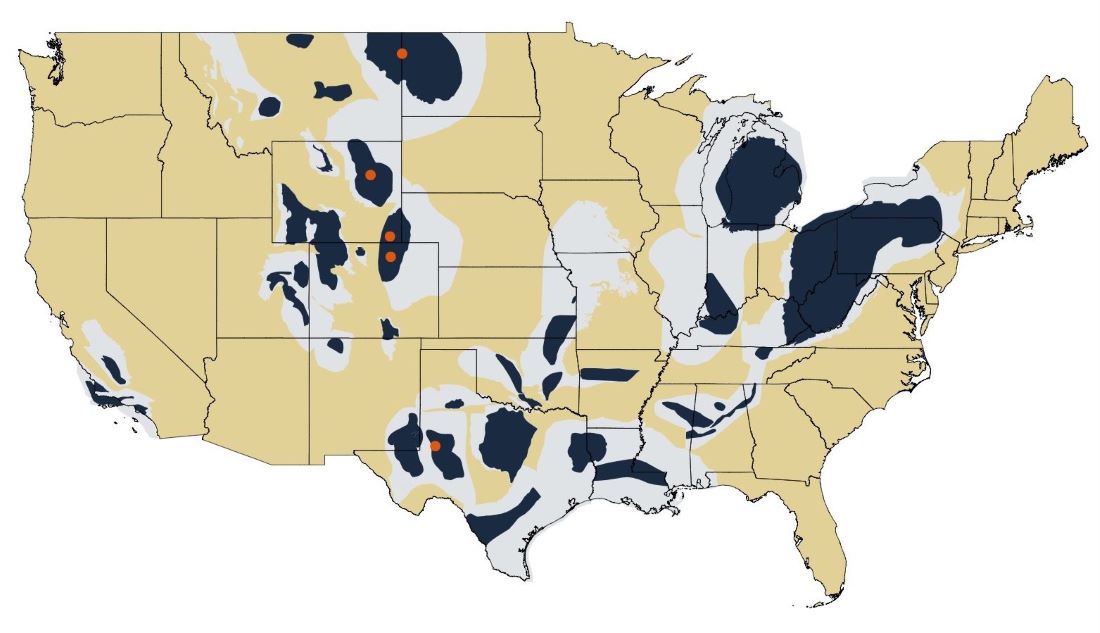

In about four years, Phoenix Capital Group has bootstrapped its way to 400 deals and developed a database of “nearly 150,000 individual records in the current markets of interest which are comprised of the key basins in North Dakota, Montana, Wyoming, Colorado and Texas,” according to a September U.S. Securities and Exchange Commission (SEC) filing.

(Source: Phoenix Capital Group)

On Nov. 10, Phoenix Capital Group purchased mineral interests in Weld and Adams counties from the city. The company said the acquisition was one of the largest mineral rights transactions in the Denver-Julesburg (D-J) basin.

Colorado, known for its political instability and sometimes open hostility toward oil and gas companies, has been an increasingly difficult state for oil and gas companies. But the Thornton deal still holds the promise of bringing in cash, Phoenix Capital Group partner and CFO Curtis Allen said. The assets the company purchased include roughly 60 drilled but uncompleted DUC wells.

“We pay up for DUCs,” he said. “That’s why we win most bids.”

The company’s due diligence team then went to work, performing on 18 tracts.

“It wasn’t actually clean. You kind of expect a city’s minerals to be pretty clean,” Allen said. “These were not. There were title flaws everywhere. But our team was able to digest all 18 tracks in less than 30 days.”

Phoenix Capital Group put 12 full-time professionals on the running title checks to get the deal closed.

“I don’t know too many other shops that could, one, take on the size of it, but, two, handle the massive amounts of due diligence as quickly as we did,” he said. “So, it kind of worked out very well.”

Disruptive business model

Allen described Phoenix Capital Group as a “wholesale shop” with a large land team looking for opportunities that aren’t heavily bid against.

“A lot of the things we’re closing are mom and dads and in the Midwest, just small families that just wanted to sell, get out of the oil game,” he said.

But the market for minerals rights remains inefficient. He pointed to the bids for the Thornton assets — Allen said there were 10 bidders but only two were “competitive.”

“On a $33 million acquisition, only two of the bids were even reasonable,” he said. “So, it’s the same thing across the nation. It’s a relatively inefficient marketplace and I think a lot of groups have taken advantage of that. They just lowball offers and hope they win.”

Despite a now sizeable portfolio with interests in 2,126 wells in the Williston, D-J and Permian, the company still sees its story as a David and Goliath tale in which the company was initially out capitalized by its peers “a hundred to one,” Lindsey Wilson, managing member and COO of the company said in a press release.

Phoenix Capital Group mineral and royalty interests as of June 2022

Source: Phoenix Capital Group SEC filing

Basin/ Region

Well count

Bakken/Williston Basin

1,875

DJ Basin/Rockies/Niobrara

164

Permian Basin

87

Total

2,126

Allen said Phoenix remains on unequal footing with public companies and private-equity-backed buyers.

“They still have more money than us, by probably a 4:1, 5:1 margin at this point. But is the gap closing? Yes. And extremely fast.”

Phoenix Capital Group has developed what it calls a disruptive business model that empowers sellers.

“We’ve made it our personal mission to change this space permanently and for the benefit of the community,” Allen said. “By changing the traditional capitalization sources and creating an honest, fair and efficient process, we are changing the mineral owner’s experience from the ‘used-car lot’ feel they’ve traditionally been force-fed, to a transparent and high-touch partnership that Phoenix Capital Group is offering.”

Allen said one competitor has tried to snuff out the competition and called the Phoenix Capital Group’s reputation into question with “slanderous information.”

“Every time we do see these people in the field in terms of a bidding war, we’ll always win,” he said, declining to name the company. “We tend to run into them a lot.”

‘Acquisition machine’

Phoenix Capital Group was formed in April 2019 by Lion of Judah Capital LLC, a family office in Chicago to purchase mineral rights and non-op working interests primarily in the Williston, Permian, Powder River and D-J basins, according to a September filing with the SEC.

Since then, the company had closed 400 unique transactions as of November, picking up speed each year. About half of all its transactions have closed this year, Allen said.

“Phoenix itself is an acquisition machine. That’s what it truly is,” Allen said. “It’s been built to find the next opportunity, the next place to put money to work.”

The company has three offices: its executive team is based in Irvine, Calif.; its acquisitions, operations and capital markets team is based in Denver; and its land team is mostly based in Casper, Wyo.

The company employs about 100 people, including 70 contractors and land personnel who “are doing nothing but scouring for the next opportunity, whether that’s from a mom and dad or from something as big as a city,” Allen said.

While the company has spent roughly $130 million to $140 million in transactions so far, Allen estimated that next year the company will deploy another $200 million in 2023. Since 2019, the company acquired 1,286 mineral assets and retained 1,020 as of September, according to its SEC filing.

“It’s definitely a company that’s gaining a ton of steam,” Allen said.

Phoenix Capital Group Acquisitions as of June 2020

Source: Phoenix Capital Group SEC filing

Acquisition Costs

Six months ended June 2022

2021

2020

Proved ($MM)

$23.50

$26.69

$2.95

Unproved ($MM)

$0.19

$0.34

$0.51

Development Costs ($MM)

$16.07

$8.25

$9.98

Total ($MM)

$39.77

$35.29

$13.45

However, because the company eschewed private equity funding when it began, it’s been slow going and, at times, forced the company to part with some assets for funding.

Private equity

Allen said he doesn’t hold anything against the public or private-equity model for mineral and royalty buyers, but he also saw the long-term consequences had the company struck a deal for that financing.

“If we went to private equity in 2019, they probably would have said, ‘You guys are worth $20 million. We’ll take 50% of your company for $10 million.’”

With the most recent valuation of its properties at close to $300 million, Allen likens Phoenix Capital Group’s scale to Brigham Minerals, which has a $2 billion market cap.

“Had I taken the equity pill in 2019 for $10 million … those private equity guys would be staring down [at] $700 [million], $800 [million], $900 million, and all they gave me was $10 million?” he said. “So it was a calculation at the very beginning, ‘do we think we can do this?’ It’s extremely difficult. I’ve been running at what I feel like is a hundred miles an hour for the past four years.”

Ambition: growth

If commodity prices don’t collapse and the company continues to execute on its core strategy, Allen said Phoenix could become “the biggest mineral shop in the United States in probably two years.”

The company isn’t thinking of an exit any time soon, which Allen said is another pitfall of private-equity-funded firms that have a set timeframe until they are required to sell. Phoenix Capital Group’s business model takes it to take all cash flows from its assets and roll them into the next asset.

“So all the free cash flow that we’ll generate in 2023, which should be substantial alongside the additional debt that we’re raising through our investor program, will all be deployed to the next asset,” he said.

(Source: Phoenix Capital Group)

“Phoenix itself is an acquisition machine. That’s what it truly is. It’s been built to find the next opportunity, the next place to put money to work.” – Curtis Allen, Phoenix Capital Group

Selling the company would be a “bad outcome,” he said. The company has developed a database of “nearly 150,000 individual records in the current markets of interest which are comprised of the key basins in North Dakota, Montana, Wyoming, Colorado, and Texas,” according to its SEC filing.

“Everything we’ve done to date from 2019 to date, which is to build that [database] software out, build the land team out, build the processes and plans … is to find the next acquisition,” he said. “That’s the true value of Phoenix. It’s not the assets we’ve already bought. The true value is the asset I’m about to buy, right?”

The company could eventually go public, but that’s not on anyone’s mind just yet, he said.

“The only really truly logical exit would be going public, which is essentially taking Wall Street’s money and applying it through our machine that we’ve created for the next opportunity,” he said.

And Allen said Phoenix feels good about providing a 9% yield to the “Midwest Main Street folks” that it sells to.

“I don’t want to crap on the private equity guys or the [investment] banks or anybody in the middle world of finance,” he said. “But I love going around them. I love going directly to Main Street folks and giving them good returns.”

{kind=link}